MiCA Full Enforcement Meets GENIUS Act Countdown

- BECTRA

- 1 day ago

- 2 min read

· ESMA conf

irmed end of 18-month CASP transitional period on July 1, 2026.

· All MiCA-licensed exchanges (Coinbase, Kraken, Binance, OKX, Crypto.com, Revolut) delisted/restricted USDT for EU users.

· Tether declined MiCA authorization — 60% EU bank deposit reserve requirement incompatible with U.S. Treasury model.

· Circle's EURC and USDC dominate compliant market, backed by ACPR EMI license (France).

· ESMA’s EMT register currently records 21 distinct issuing entities across 12 EEA jurisdictions—including 11 EU Member States and Iceland—and 41 EMT white-paper/register entries.

· Only ~12% of EU crypto firms obtained MiCA authorization.

· Six federal agencies (FinCEN, OCC, FDIC, Fed, SEC, CFTC) must finalize stablecoin framework rules by July 18, 2026.

· Rules govern stablecoin issuance, reserve management, AML/CIP requirements.

· Federal Reserve timeline concerns — potential 'GENIUS Act Fed Gap' if Fed rules lag.

· Compliance cost estimated at ~$15M annually for mid-sized issuers.

MiCA's 60% EU bank deposit reserve requirement (designed for consumer protection) made USDT authorization commercially unviable for Tether, which declined. Circle, holding the ACPR license, now faces near-zero compliant competition in the EU regulated market. EU officials have already opened MiCA 2.0 consultations to address concerns that reserve rules 'handed Circle a monopoly.

Implication: MiCA inadvertently created a regulatory moat for a single US-domiciled issuer. French ACPR, which granted the license enabling this concentration. The correction (MiCA 2.0) may take 18-24 months.

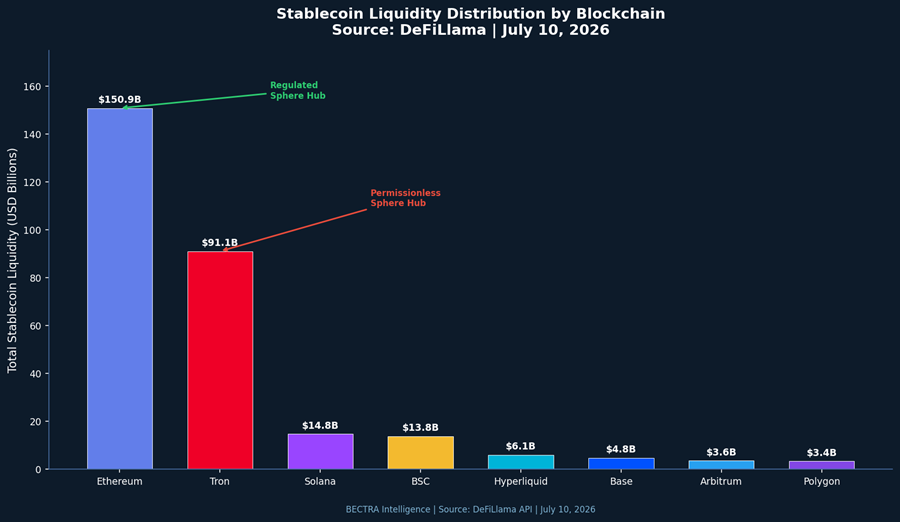

Ethereum hosts $150.9B in stablecoins (Regulated Sphere hub); Tron hosts $91.1B (Permissionless Sphere hub, almost entirely USDT). USDT on Tron is the primary cross-border payment instrument in @UEMOA/CEMAC — up to 90% cheaper than traditional banking. BEAC joined PAPSS in July 2026 to reduce foreign currency dependence.

Implication: MiCA enforcement is pushing USDT deeper into the Tron/emerging market ecosystem, paradoxically strengthening the permissionless sphere. Bifurcation is not just geographic but infrastructural (Ethereum vs. Tron).

GENIUS Act signed July 18, 2025; six agencies have until July 18, 2026 to finalize rules. Federal Reserve timeline concerns suggest potential 'Fed Gap.' UK FCA published final stablecoin rules July 7, 2026 — capital charge halved to 1%, gateway opens Sept 30. EU MiCA 2.0 consultations launched in response to GENIUS Act.

Implication: a regulatory race between EU, US, and UK for stablecoin market leadership. UK's more lenient framework (1% vs. 60% bank deposit) may attract issuers seeking compliant but less restrictive European base. Blind spot: UK post-Brexit regulatory arbitrage is underestimated.

12 European banks backing Fireblocks for MiCA-compliant euro stablecoin. Major banks (Standard Chartered, BNY Mellon) moved beyond pilots to offer USDC minting/custody. Crypto card volume surpassed $10B cumulative (+82% YTD). SG-FORGE (EURCV) holds MiCA authorization with €129.5M in circulation.

Implication: traditional banks are positioning to issue and distribute stablecoins directly. The 12-bank Fireblocks consortium, if confirmed, would challenge Circle's EURC dominance from within the regulated sphere. Silent Actor : European banking consortia as the 'dark horse' in the MiCA-compliant stablecoin race.

Comments